After years of slow transition, biomanufacturers are finally ranking disposable bioprocessing as their top factor creating improvements in their biomanufacturing performance, according to BioPlan Associates’ latest study, 12th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production1. But most of this enthusiasm for these disposable, typically plastic, single-use devices has come from upstream bioprocessing, including bioreactors, mixing systems, and basic storage functions. Improvements on the downstream purification side have so far failed to make the same impact. And until a full chain of single-use operations is in place, the total benefits of an integrated single-use facility won’t be realized.

Our annual study continues to indicate widespread dissatisfaction with current downstream purification, and a desire for less costly, more disposable product innovations.

Separate research we have conducted shows that while upstream productivity, measured by titer and yield improvements, have grown by as much as 10 fold during the past decade, on the downstream side, improvements in factors like processing yield at commercial scales has only doubled, at best. The progress in upstream productivity, in combination with stalled progress in downstream performance has put significant pressure on downstream operations. Given that historical backdrop, it’s not surprising that our study finds the pressure on downstream processing advances to be the second-most critical biomanufacturing trend. This is the area that the industry feels it must focus its efforts on this year–this relates to the overall demand for general manufacturing productivity and efficiency. In fact, the interest in downstream processing advances has overtaken other major factors like manufacturing cost reductions and even biosimilars in importance over the past year.

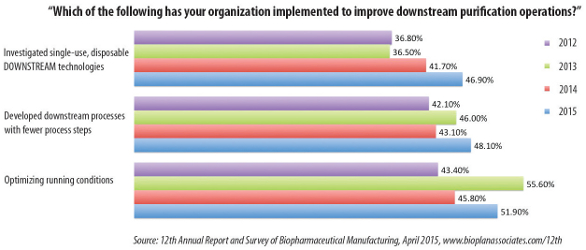

Figure 1. Improving Downstream Operations, 2012-2015, Select Responses

Figure 1. Improving Downstream Operations, 2012-2015, Select ResponsesSingle Use Having an Impact

Study results suggest that single-use devices are having some impact on downstream processing. This year, almost half (46.9%) of our survey respondents said that they had investigated single-use disposable downstream technologies in order to improve downstream purification operations, up from 36.5% just a couple of years ago. Among CMO respondents, this was the leading factor behind improved downstream operations; CMOs, not developers, are taking the lead in the adoption of new or streamlined DSP approaches, with CMOs much more incentivized and motivated by cost-savings and associated need to develop and adopt standardized manufacturing platforms.

Chromatography Steps Blamed; Alternatives Lacking

For at least the past 12 years, our research from multiple studies indicates that Protein A resin chromatography is a significant bottleneck step in downstream purification. The ‘problem’ is that it is quite costly, and sometimes difficult to manipulate, pack, and work with. The good news is that it works remarkably well for purifying proteins, and it doesn’t raise eyebrows among regulators, who are generally quite happy with it as a unit operation. However, that doesn’t mean it isn’t creating bottlenecks. A worrisome 44% of respondents reported moderate to severe capacity constraints at their facilities due to chromatography columns, compared to 31% facing constraints due to depth filtration and 28% from ultrafiltration steps.

As a result, the industry is clamoring for new product development in this area, with chromatography products (36%) and disposable purification products (36%) jointly topping the list of innovation areas where the industry is pressuring suppliers to focus their R&D efforts.

Figure 2. New Downstream Processing Solutions, Select Responses

Figure 2. New Downstream Processing Solutions, Select ResponsesFor the time being, single-use alternatives to chromatography aren’t topping the list of new downstream technologies in consideration by end-users. Partly because none really exist for large scale operations, although a number of suppliers are developing alternatives, so this situation is likely to change in the near future. Of the 21 current ‘novel’ technologies being evaluated by end users, this year’s top DSP technologies being considered are:

- Use of high capacity resins (50% considering, down from 52.1% last year);

- Continuous purification systems (50%, up from 32.4%)

- In-line buffer dilution systems (43.4%, up from 39.4%)

A little further down the list are single-use prepacked columns (36.8%) and alternatives to chromatography. Besides lack of progress in terms of process efficiency, chromatography and Protein A resins have largely resisted development within singleuse systems, a major long-term problem. Despite its costs, the ability to in-house recycle Protein A-based resins for antibody purification continues to dominate DSP. But interest in alternatives of all sorts continues to grow. In fact, according to Dr. Kiran Chodavarapu, Business Development Manager, W. R. Grace & Co.:

“There continues to be a very high level of interest in innovative single-use chromatography solutions. As more complex mAbs and biosimilars are developed, especially where cost control is critical, prepacked disposable chromatography columns offer solutions to accelerate clinical trials. There are a growing number of downstream SUS options and I expect that the journey is not over in this space.”

That transformation could indeed take some time, as even when better, more cost-effective, single-use equipment becomes available, it can be difficult to adopt. It is generally difficult to make major changes in bioprocesses, and there is inherent conservatism and slowness to adopt anything new in the highly regulated bioprocessing industry. This reluctance is compounded by the fact that there remain few feasible alternatives and there are currently no clearly proven technologies at any large scale and even fewer having advanced to adoption for commercial manufacturing, such that they are used (approved) for GMP commercial products manufacturing. Advances in single-use relating to Protein A are most commonly seen in pre-packed single-use columns. These single-use devices (which are reportedly often re-used anyhow) have grown in adoption in recent years: This year’s study shows that 36.8% are considering them this year, up from 27% in 2013 and just 1% in 2010.

Can Suppliers Deliver?

The good news is that industry suppliers are aware of the limitations of current practices and some are working to meet them. When we surveyed suppliers to the industry on the top technologies their companies are working on, we found disposable chromatography, continuous chromatography and alternatives to Protein A to be in the top half of new products in development. Even so, none of these products were in the top five development areas. Given manufacturers’ focus on downstream processing advances and chromatography bottlenecks, we might assume that they would want downstream advances to be higher on the list of suppliers’ efforts.

WL Gore’s Dr. Chodavarapu doesn’t believe that the industry has become acclimated to the problems of using Protein A, noting:

“The problems and cost of Protein A chromatography are still painful, and I do not believe the market has become numb to it. However… new products now offer more options to customers who might need higher flow capabilities or sometimes, just lower cost Protein A resins.”

Conclusion

Results from our latest industry study suggest that downstream processing problems are yet to abate. That could prove to be an opportunity for suppliers with innovative new products that will address cost, throughput, and ease-of-use issues, and that will be acceptable to regulators. Though the pace at which new products can be adopted and implemented is often slow, the rapid and widespread penetration of single-use upstream products in recent years suggests that acceptable downstream alternatives to current chromatography will be well received. Advances being made in device engineering, in lower cost Protein A options, and in other filtration suggest a positive outcome for the current bottlenecks. Until then, downstream fixes will continue to remain incremental, and based on optimizing current operations.

References:

- 12th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, April 2015, Rockville, MD www.bioplanassociates.com/12th

Author Biography

Eric S. Langer is president and managing partner at BioPlan Associates, Inc., a biotechnology and life sciences marketing research and publishing firm established in Rockville, MD in 1989. He is editor of numerous studies, including “Biopharmaceutical Technology in China,” “Advances in Large-scale Biopharmaceutical Manufacturing”, and many other industry reports. [email protected] 301-921-5979. www.bioplanassociates.com