Introduction

Biosimilars are continuing to change the biopharmaceutical industry. Some biosimilars and biogeneric products have already entered world markets, and the rather full development pipeline1 means many more are coming, along with many new entrants into the biopharmaceutical industry. This article reviews aspects of the biosimilars’ development pipeline and some of the changes biosimilars are promoting within the biopharmaceutical industry, particularly changes in biopharmaceutical manufacturing (bioprocessing).

A large number of biosimilars are in development worldwide.1,2 ‘Genuine’ biosimilars tend to be follow-on biologics in more developed and highly regulated countries that undergo rigorous and extensive analytical and clinical testing, including in direct comparison with their reference product, the established biopharmaceutical each biosimilar seeks to ‘copy.’ Biogenerics, often cited as ‘biosimilars,’ are a subset of biosimilars generally distributed in lesser- and non-regulated international commerce. They typically lack rigorous (and very costly) analytical and clinical testing, including comparisons with reference products; and not manufactured to GMP standards.3 Biosimilars are only marketable after the expiration periods of government-granted exclusivities of the reference products each emulates, whether based on patents, approvals- or orphan products-related exclusivities. In this context, the biosimilars entering world markets mark the maturing of the biopharmaceutical market.

Subscribe to our e-Newsletters

Stay up to date with the latest news, articles, and events. Plus, get special offers

from American Pharmaceutical Review – all delivered right to your inbox! Sign up now!

Much like drugs (chemical versus biotechnology manufacture), biopharmaceuticals are now becoming subject to generic drug-like competition. Like generic drugs, the requirements for biosimilar approval (in more highly-regulated countries) are less cumbersome and costly compared to mainstream innovative therapeutics, which are now reported to cost on average over $2 billion each to bring to market. Biosimilars can be brought to market for an order of magnitude less cost, e.g., several hundred million dollars, with some claiming costs are much less. Biosimilars involve considerably less supporting research, can rely on published literature for much of this; and less clinical testing, generally avoiding costly large Phase III trials in favor of direct comparison trials with the reference product; and manufacturing not at GMP standards. Biogenerics are essentially all developed by companies in, and the products targeted to, lesser- and non-regulated domestic and international markets. Biobetters are another related class of follow-on biopharmaceutical products related to biosimilars involving different, not targeted to be copies or even biosimilar, variations of existing products, with the product’s active agent’s primary structure retained but with some other molecular (e.g., pegylation) or finished product modifications (e.g., oral vs. injected format). Biobetters are new, different, and innovative.

Patents Control Marketability

There are currently over 1,000 diverse biosimilars in various stages of development.1 Analysis of the projected expiration dates for U.S. patent, orphan and original approvals-related exclusivity periods shows that patents are, by far, the main determinant of when biosimilars can enter the market.4 This is contrary to the assertions of many, including activists and politicians, that shortening the current 12-year period of FDA reference product approvals-based exclusivity will result in more biosimilars entering the market earlier. However, this ignores U.S. patents, which now have 20 years post-filing pendency, with essentially every reference product well protected by one or often more patents.

Examination of over 100 reference products’ exclusivity periods has shown that patent protection extends beyond the 12-years approvals’ exclusivity 87% of the time, with an average pendency period of 15.8 years; with patent protection extending beyond 7-year orphan exclusivity 96% of the time, and beyond 5-year New Chemical Entity (NCE)-granted exclusivity 100% of the time. Thus, shortening any exclusivities other than patents will have no real impact on U.S. biosimilar market entry. There was a wave of biosimilars that became marketable (patents expired) around 2013-15 with another wave of expected approvals now starting. In the mid-term, e.g., ≥5 years, as patents expire and the pipeline matures, biosimilars will come to outnumber mainstream (recombinant) biopharmaceuticals in the U.S. and other markets worldwide. This will obviously have significant impact on the (bio)pharmaceutical industry, besides providing more competition.

Biosimilars Pipeline Analysis

The current follow-on products (biosimilars and biobetters) pipeline is summarized in Table 1, with biobetters data for comparison. These and other data are derived from the Biosimilars/Biobetters Pipeline Directory which cumulatively tracks all follow-on products in development worldwide.1 Coverage includes only mainstream, nearly all recombinant, proteins and antibody products, with vaccines, cellular, and blood/plasma-derived products excluded. There are over 1,000 such biosimilars in the pipeline, with ≥40% being biosimilars initially targeting major, generally highly-regulated, markets. This includes ~80 biosimilars in major markets either approved or with pending approvals (although many of these are biosimilars of the same reference products). The other ≤60% in the pipeline are diverse biogenerics initially targeting lesser-developed country markets. Keep in mind, biogenerics can often be readily upgraded with needed testing done and manufacturing brought up to GMP, and receive biosimilar approvals in major, developed country markets.

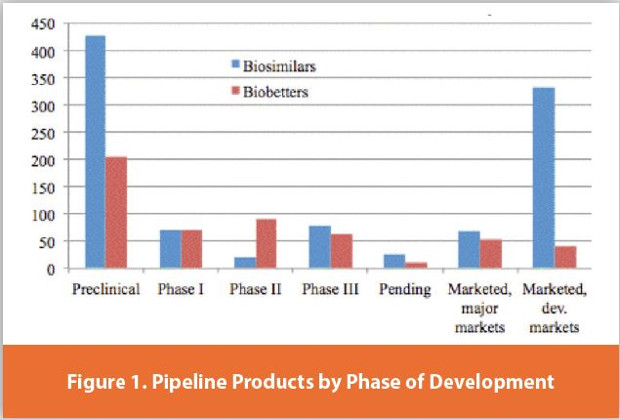

The current stages of development of the follow-on pipeline is shown in Fig. 1. The great majority of products, as is normal, are in preclinical development. The “Marketed, Developing Markets” category captures biogenerics, with over 300 of these already in their home country’s and/or international commerce. These products are often brought to market very quickly, e.g., marketed based on their simply meeting minimal pharmacopeia specifications, with these products generally having relatively small markets compared to major market biosimilars. With biobetters involving some innovation and requiring full, not biosimilar, approvals (costing more to develop), the number of pipeline products is more limited.

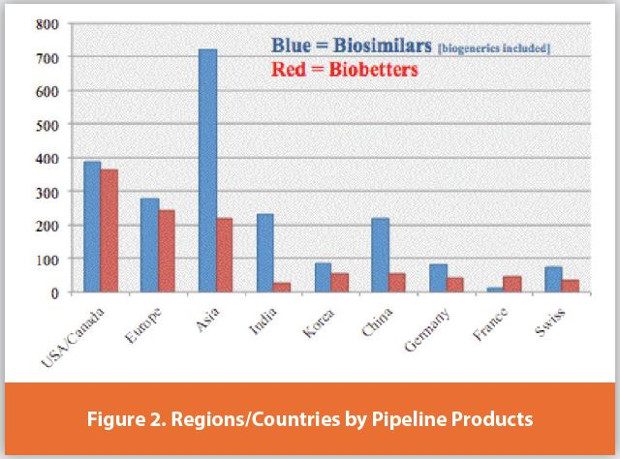

The distribution of follow-on products development based on the location (headquarters) of the developer is shown in Table 2. Numerically, most marketed biosimilars originate from countries in Asia, nearly all from India or China, with nearly all of these biogenerics in regional and international markets. A good number of these biogenerics can be expected to sooner or later be launched into major markets as biosimilars, especially those from China which is working toward this, while Indian developers primarily target domestic and international biogenerics markets. The largest portion of ‘genuine’ biosimilars originate from U.S. developers, followed closely by Europe, with essentially none of these developers initially targeting their products to developing countries, many of which can only afford biogenerics (if that). In terms of specific countries having biosimilars in the pipeline, the leaders are the U.S.; India and China nearly tied; South Korea and Germany nearly tied; closely followed by Switzerland. The U.S. is fully expected to be the source for the largest portion of biosimilars, with it still the leader in (bio)pharmaceutical research, development, and with the largest biopharmaceutical market (~50% of the world market). The impact of biosimilars in the U.S. will increase dramatically as the U.S. slowly catches up with Europe, with the European Union (EU) currently having the most approved ‘genuine’ biosimilars.

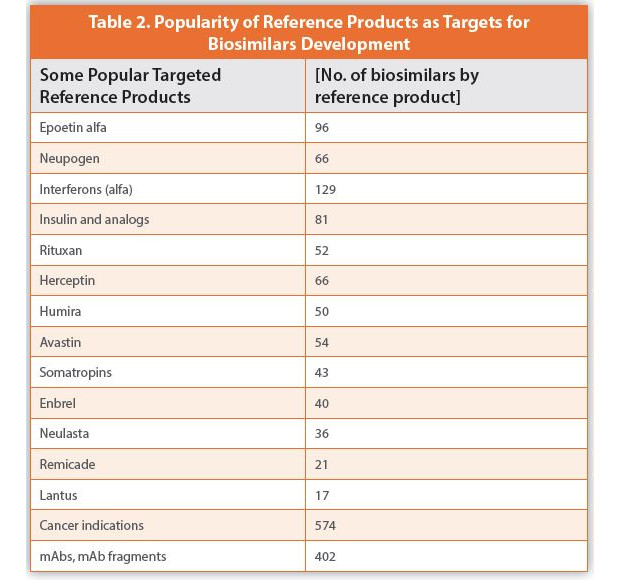

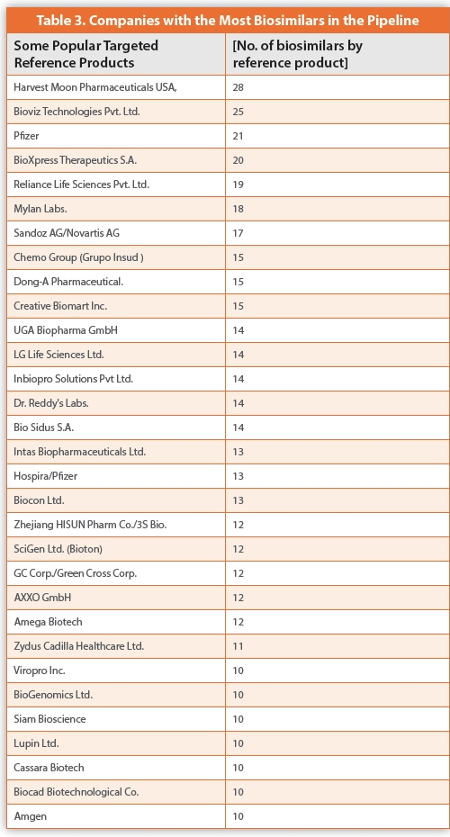

Biosimilars in the development pipeline generally correlate with the sales of their references products. This includes a large number of biosimilars targeting the same ‘popular’ reference products, particularly the ~50 blockbuster (≥$1 billion/year) biopharmaceuticals. Table 2 shows the number of biosimilars in development worldwide targeting specific or classes of reference products. From this, Amgen is the most biosimilars-threatened reference products manufacturer, with nearly 200 biosimilars targeting its epoetin alfa products (Epoetin, Procrit), Neupogen, and Neulasta. In terms of indications (diseases) targeted the largest number are cancer therapeutics; and over 400 biosimilars, ≥40%, in the pipeline are monoclonal antibody products. In terms of companies, those with ≥10 biosimilars in the pipeline are shown in Table 3. This shows the great diversity among biosimilars developers, ranging from small unfamiliar and developing country-based developers to the largest biopharmaceutical and Big Pharmatype companies. Eventually, a good number of biosimilars marketers can be expected to have rather large portfolios of biosimilars, e.g., over a dozen, with most of the products from the smaller companies licensed to bigger ones for marketing.

Biosimilars Impacting the Biopharmaceutical Industry

The biosimilars pipeline is having significant impacts throughout the biopharmaceutical industry. This is besides their marketing-related aspects, with biosimilars priced cheaper than their reference products and providing much more competition in the market. Biosimilars compete against products including their reference products, other biosimilars, biobetters, and other products used for the same indications. Biosimilars are having significant impact on biopharmaceutical manufacturing (bioprocessing). This includes contract manufacturing organizations (CMOs), which commercially manufacture ≤33% of biopharmaceutical products, reporting an overall 15% increase in business due to biosimilars.

Biosimilars developers need to adopt more advanced bioprocessing, in order to attain lower manufacturing costs, a significant factor determining final consumer prices. Biosimilars developers are nearly all using modern, often cutting-edge, bioprocessing, rather than seeking to fully copy their ≥20-years old reference products manufacturing methods. This includes a majority being developed using single use (disposed of after use) bioprocessing systems, not traditional stainless steel-based manufacturing. In the future, a higher portion of biosimilars versus innovative products will likely be manufactured using new continuous vs. conventional batch-based bioprocessing.

Cost of Manufacturing

Biosimilars need to be manufactured cost-effectively, with emphasis on higher productivity, yields, and speed-to-market. Manufacturing costs ideally need to be in the average or ideally much better ranges.5 The average cost of monoclonal antibody manufacturing is now in the $300/gram range, with only a few of the very largest facilities, including decades-old blockbuster manufacturing and new Korean super-sized facilities, able to attain costs about or below $100/gram.

Estimated lowest costs attained/attainable with different types of bioprocessing range from as low as $90 for certain stainless, legacy facilities to $150/gram for some developing region manufacturers. Nearly all of the “Legacy, older large stainless steel” are ≥100,000 L (onsite total bioreactor volume) facilities manufacturing blockbuster or other reference products, mostly monoclonal antibodies, where bioprocessing has been repeatedly incrementally upgraded and facilities have long been ‘paid for’ many times over. Smaller, newer, including single-use, facilities generally can manufacture at costs below $200-$300/gram (still commercially very viable, considering even low-potency monoclonal antibodies involve ≥10 patient doses/ gram). But in our recent analysis, over a fifth of facilities surveyed continued to report costs ≥$500/gram.

Competition

The nebulous nature of biosimilars’ competition (which products? from whom? when?), potentially including radical discounting of prices, makes low cost-effective manufacture of biosimilars a commercial necessity for many. The often pioneering adoption of newer bioprocessing technologies by biosimilar developers will sooner or later carry over to innovative products, with all biopharmaceuticals benefiting from increased manufacturing productivity. But reference products manufacturing costs still generally remain lower than with even the newest bioprocessing, with these manufacturers, besides incremental improvements, also having decades experience making these products at scales that dwarf biosimilar manufacturing, with associated economies-of-scale and facilities long ‘paid for’ many times over.

Biosimilars are bringing in a large number of new biopharmaceutical industry players, including a large number of smaller, new, and foreign companies (some of which may be using the production of biosimilars as an entry method to larger, or more developed markets). Big Pharma, generic drug, and other pharmaceutical companies are also getting involved in this segment. In coming years, there may be more biosimilars vs. innovative biopharmaceuticals in many countries’ markets. This will change the underlying nature and perceptions of the biopharmaceutical industry, which now is primarily promoted, e.g., by related trade associations, as being thoroughly innovative. Biopharmaceuticals’ marketing will increasingly resembling the generic drugs market, including more products and cost competition (now largely lacking). Biosimilars are also bringing in many new players, and this may lead to problems, potentially even safety concerns and high visibility liability lawsuits that the biopharmaceutical industry has generally avoided to date. These could have a significant impact on the biopharmaceutical industry if such problems occur.

References

- Rader, R.A., Biosimilars/Biobetters Pipeline Directory, online database) and derived PDF report, >700 pages.

- Rader, R.A., “Biosimilars Pipeline Analysis: Many Products, More Competition Coming”, Biosimilar Development, July 26, 2016, www.biosimilardevelopment.com/doc/biosimilars-pipeline-analysis-many-products-more-competition-coming-0001

- Rader, R.A.., “Biosimilars in the Rest of the World: Developments in Lesser-Regulated Countries,” BioProcessing J., 12(4), Winter 2013/2014, p. 41-47.

- Rader, R.A., BIOPHARMA: Biopharmaceuticals in the U.S. and European Markets, online database, www.biopharma.com.

- Rader, R.A., “Biosimilars Paving The Way For Cost-Effective Bioprocessing,” Biosimilar Development, Aug. 23, 2017.

Author Biographies

Ronald A. Rader is Senior Director, Technical Research, BioPlan Associates. He has 35+ years’ experience as a biotechnology and pharmaceutical, particularly biopharmaceutical, information specialist, analyst and publisher. Publications/information resources he has been responsible for include the Antiviral Agents Bulletin periodical; the Federal Bio-Technology Transfer Directory; BIOPHARMA: Biopharmaceutical Products in the U.S. and European Markets; and the Biosimilars/Biobetters Pipeline Directory. info@bioplanassociates.com, +1 301-921-5979, www.bioplanassociates.com

Eric S. Langer is President and Managing Partner at BioPlan Associates, Inc., a biotechnology and life sciences marketing research and publishing firm established in Rockville, MD in 1989. He is editor of numerous studies, including “Biopharmaceutical Technology in China,” “Advances in Large-scale Biopharmaceutical Manufacturing”, and many other industry reports. elanger@bioplanassociates.com, +1 301-921-5979, www.bioplanassociates.com.