Introduction

Single-use or disposable bioprocessing equipment is now used for ≥85% of pre-commercial scale, i.e., preclinical and clinical, biopharmaceutical manufacturing, and is increasingly being adopted for commercial products manufacturing.1 Are the dinosaurs, i.e., classic large scale fixed stainless steel equipment-based bioprocessing facilities, such as the many facilities now producing biopharmaceuticals using one or more ≥10,000 L bioreactors, becoming extinct? Not quite yet, but with single-use (disposable) bioprocessing systems already dominating the pre-commercial market and a trend for increased adoption for commercial scale manufacturing, in many respects, single-use will soon dominate much of biopharmaceutical manufacture, particularly at other than large scales. Most commercial biopharmaceutical manufacturing, particularly high volume products, will continue to use fixed stainless steel systems, as this often remains economically more feasible at large scales. But single-use facilities will come to dominate bioprocessing in terms of number of facilities, process lines, bioprocessing professionals’ work, and the number of products manufactured, especially at clinical scales. These projections come from the BioPlan Associates’ 15th Annual Survey on Biopharmaceutical Manufacturing Capacity and Production.1 We further project a rapidly growing SUS market exceeding $10 billion/year in 5 years.

Single-use systems (SUS) refers to biopharmaceutical manufacturing (bioprocessing) equipment designed to be used once (or for a single manufacturing campaign) and then discarded.1 Generally, SUS equipment is composed primarily of plastic components that have been sealed and sterilized using gamma irradiation. The primary benefits of SUS versus classic stainless steel (or glass less frequently used in bioprocessing) is that the equipment comes sterile, allowing avoidance of cleaning, sterilization and validation of sterilization prior to usage; and avoidance of related complex steam, WFI, and other plumbing installed throughout bioprocessing facilities with large fixed stainless steel components. With SUS equipment essentially plug-and-play, process turnaround and set up of new processing lines are much quicker, avoiding weeks of cleaning/sterilization/validation required with reused stainless steel equipment. Also, with much less facility infrastructure required, including no need for a lot of plumbing or an in-house WFI plant, and with bioprocessing suites as simple as empty rooms to be filled with a SUS-assembled process line, the facility footprint can be much smaller, investment and construction costs much lower, and new process lines and facilities come online much faster and simpler versus stainless steel. However, SUS bioprocessing requires continued, repeated expenditures to purchase new equipment, often whole process lines, after their single use (or use for a single campaign, i.e., repeated use for manufacture of API to be combined into a single lot/batch).

Subscribe to our e-Newsletters

Stay up to date with the latest news, articles, and events. Plus, get special offers

from American Pharmaceutical Review – all delivered right to your inbox! Sign up now!

Despite repeated purchase for lot/batch and the SUS supplies for each larger-capacity process lines generally costing millions of dollars, industry consensus has now developed that accepts SUS based bioprocessing as generally cheaper, simpler, and preferred over use of stainless steel, at all but the largest scales and commercial manufacturing.1,2 The costs for repeated purchases are generally more than compensated by the avoidance of cleaning/sterilization/validation, related time lost, and the loss of flexibility that comes with stainless steel facilities. We discuss below SUS History, Status and Trends, and recent trend data published in BioPlan Associates’ 15th Annual Survey on Biopharmaceutical Manufacturing Capacity and Production (see: www.bioplanassociates.com/15th).1 This survey included responses from 352 individuals, including 222 working for biopharmaceutical developers/manufacturers, and 130 working for bioprocessing suppliers or vendors.

SUS History, Status and Trends

A few types of legacy SUS products have long been used in bioprocessing and many other industries, notably filter membranes and silicone tubing. However, modern SUS, with nearly all bioprocessing equipment available in SUS format, did not really get started until the early-mid 2000s, with most growth and adoption in the past decade. For example, GE acquired WAVE bags, then the leading SUS bioreactor product line, in 2007, with this the first major move by a major bioprocessing supplier into the SUS market. As discussed below, the SUS market has grown dramatically in the past decade.

The current SUS paradigm for much of the critical equipment, such as bioreactors, mixers and diverse containers used throughout bioprocessing, involves a SUS bag/liner held within a stainless steel or other rigid container. The plastic films/bags used are generally composed of multiple, laminated or fused layers of different polymers, such as an inert inner contact layer, a layer to block oxygen/gas transfer, a layer for tear-resistance, a “tie layer” or adhesive between layers, etc. Films/bags are often composed of six or more layers. Only very recently have single-layer, unitary SUS films/bags been introduced. However, this bag-in-container paradigm includes a number of inherent practical limitations, particularly size/scale/volume. SUS bags and their containers are unwieldy and difficult to install and move at large scales. 2,000 L is the current practical limit for scale of SUS equipment, with 2,000 L of fluid (528 gallons), volume comparable to 10 x 55-gallon drums, and weighing ~2,000 kg (4,400 lb.). In contrast, stainless steel bioreactors and containers ≥5-10,000 L each are currently commonly used for commercial scale manufacturing, often with multiple such bioreactors being used. With advances in bioprocessing technology, notably steadily increasing upstream productivity (discussed below), multiple 1,000-2,000 L SUS bioreactor-based systems in parallel, or even a single system, can now often compete with stainless steel and produce enough to supply commercial markets.

Thus, SUS equipment is primarily used up to the 2,000 L scale, with this generally supporting pre-commercial manufacturing (preclinical and clinical supplies), but usually not commercial manufacturing. Besides the advantages of SUS, most commercial scale manufacturing remains more cost effective using purpose-designed stainless steel facilities.

Multiple SUS systems used in parallel can produce products at costs that are still competitive, allow considerable profit, such as $300-$500/kg of recombinant protein. But the largest-types stainless steel facilities can attain much more economies-of-scale, and can provide product at costs as low as ≤$100/gram, the current lowest costs being attained in the industry.3

SUS use is primarily confined to mammalian cell culture, now the predominant bioprocessing technology, including use for manufacture of ≥66-70% of biopharmaceutical products. The availability of SUS equipment has contributed to the popularity of mammalian-based bioprocessing. Microbial bioprocessing, used for manufacture of nearly all other products, has resisted SUS implementation, with fermentation performed at higher temperatures, pressures, much more energetic mixing, etc. compared to mammalian cell culture.

Some suppliers have launched SUS microbial bioreactor process lines, but these have not seen much adoption.

The past decade has seen adoption of SUS equipment and process lines adopted instead of stainless steel-based systems. An estimated ≥85% of current pre-commercial (sub-commercial scale) bioprocessing now involves full or considerable use of SUS, at least upstream. At other than large scales, SUS is now generally preferred and presumed cheaper than use of stainless steel. With pre-commercial manufacturing only done intermittently, as needed over years of product development, and involving smaller quantities, the total capacity and the volume (kgs.) of products manufactured using SUS are relatively small compared to stainless steel-based manufacturing. For example, >97% of the total world’s bioprocessing capacity (cumulative bioreactor volume), now estimated at about 16.7 million L, is at facilities with over 2,000 L on-site capacity.2 Despite sub-2,000 L bioreactors being dominant in terms of numbers, these are only a very small portion of total bioprocessing capacity, with capacity dominated by bioreactor stainless steel-based commercial manufacturing facilities.

Downstream processing, primarily purification, has resisted adoption of SUS. Chromatography columns and resins and other purification methods are currently rarely cost-effective as SUS, with columns and resins generally reused/recycled multiple times. Just the cost of Protein A resin used for initial recombinant antibody capture at any larger scale can be millions of dollars, too costly for this to be discarded when it can be readily reused. The industry may have to wait for new chromatography and other purification technologies more suitable for single-use to have better options for downstream SUS bioprocessing, such as perhaps the multi-column continuous chromatography systems now starting to enter the market. But until then, most chromatography and other downstream processing will involve reuse vs. single-use.

Nearly all commercial manufacturing of biopharmaceuticals to date has involved use of stainless steel-based process lines and facilities. But this is starting to change, with some new facilities implementing multiple 1,000-2,000- L SUS bioreactor-based systems in parallel to manufacture comparable amounts of product. Such adoption of SUS for commercial manufacturing will increase dramatically in coming years. However, we do not foresee the majority of new commercial biopharmaceutical manufacturing capacity to be single-use for quite some time, likely at least a decade. At the very largest scales, fixed stainless steel facilities will continue to be more cost-effective and used. Many large legacy stainless steel commercial facilities, such as those manufacturing blockbuster monoclonal antibody products, continue to manufacture products in the range of the lowest costs attainable per gram.

A trend that has supported SUS adoption has been the constant increase in bioprocessing productivity, particularly upstream titers (concentration of product produced per bioreactor volume).4 Back in the 1980s, with the first recombinant products entering the market, mammalian cell culture titers were in the few tenths of a grams/L range. But titers have steadily, incrementally grown such that the average reported titers with both new clinical and commercial bioprocesses is now 3.4 grams/L.1 However, in the same approximately three decades, average downstream yields have not increased much, from 70% to now about 75%. This over an order magnitude intensification of bioprocessing, particularly upstream, has greatly facilitated SUS adoption, with much smaller scale equipment now usable for manufacture of the same or even more amounts of product.

A decade or more ago, manufacture of several 100 kg/year of a monoclonal antibody, often sufficient for a niche or biosimilar market, would have required multiple 5,000-10,000 L or larger stainless steel bioreactors runs and other comparably-scaled equipment. But now, the same amount or more can be manufactured with a few or even one 500-2,000 L SUS bioreactors quicker and often at lower cost.3 Contract manufacturing organization (CMO) facilities have been and will continue to be leaders in SUS adoption, with CMOs needing the rapid turnover and flexibility SUS provides.1 BioPlan tracks bioprocessing facilities worldwide and provides the free Top1000bio.com Web site [see www.top1000bio.com] reporting data from the largest 1,000+ facilities.2 Total worldwide bioprocessing capacity is estimated to be ~16.7 million L. An estimated <7%-10% of current worldwide total bioprocessing capacity, or <1.7 million L capacity, involves primarily SUS process lines, with stainless steel dominating largest volume production. Regional use of SUS generally parallels regional bioprocessing capacity, but with increased use of SUS in developed versus developing countries. Between high import duties on equipment, lacking experience with SUS, and there often being domestic sources for stainless steel systems, bioprocessing in developing countries, including China and India, will continue to be dominated by stainless steel, even at sub-commercial scales. The limited nearterm adoption of SUS in developing countries is primarily associated with company plans to sooner or later bring products to developed markets using familiar stainless steel. For example, companies in China developing products for the US/EU markets are tending to adopt SUS, including for eventual GMP commercial manufacturing.5 The over 150 companies worldwide involved in biosimilars (and related biogenerics in developing countries) are another pool of developers that will include most adopting SUS to facilitate their attaining full GMP and major market approvals, with this adding a large number of SUS commercial product manufacturing facilities.3

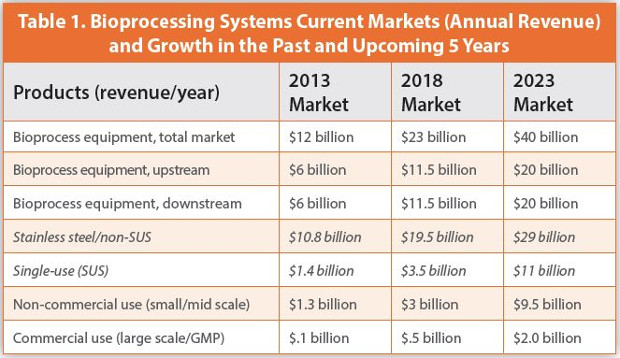

Market Size and Trends

Total worldwide bioprocessing capacity (as cumulative bioreactor volume) has grown steadily in recent decades, and will continue to grow, generally following the ≥12% annual growth in biopharmaceutical revenue (and most other relevant parameters). BioPlan Associates now estimates total worldwide capacity at about 16.7 million Liters.2 BioPlan’s estimates for SUS and related markets are shown in Table 1. With total biopharmaceutical product revenue about $275 billion/year, the overall bioprocessing supplies market is currently about 8% of this total. BioPlan estimates that commercial biopharmaceutical product manufacturing costs average about 4%-6% of product revenue. SUS equipment/facilities currently involve ~15% market share, revenue-wise, and is projected to change in 5 years to about a 72% stainless/28% SUS split. As can be seen, growth in sales of SUS supplies has been and will continue to be rather dramatic, including in the next five years. With the pre-commercial SUS market essentially saturated, much upcoming growth will be from new process lines and facilities adopting SUS for commercial manufacturing.

Market Perceptions and Growth

The annual survey of biopharmaceutical manufacturing professionals by BioPlan Associates is now in its 15th year. This confirms that among the facilities surveyed, mostly in U.S. and Europe, average facility purchases of single-use equipment are now over $1 million/year. Bioprocessing professionals recognize that SUS has improved bioprocessing. Over two thirds (68.8%) of survey respondents this year cited SUS as providing “some” or “significant” improvements in their bioprocessing within the past year.

Figure 1 shows the average responses from developer survey respondents reporting use of various SUS equipment at their facility.

Relatively inexpensive consumables, e.g., tubing and filters, lead in terms of frequency of use, but it is significant that over 75% report use of SUS bioreactors, indicating likely full(er) use of SUS.

The leading reasons cited as “very important” resulting in adoption of SUS were:

- “Decrease risk of cross-product contamination” cited by 46.2%;

- “Eliminating cleaning requirements” 41.2%;

- “Reducing time to get facility up and running” 44.1%; and

- “Reduce capital investment in facility & equipment” 40.4%.

Year-after-year respondents cite much these same money, risk, time and cost reduction reasons.

The top 5 downsides or potential problems with SUS, those cited by >50% of respondents, were:

- “Breakage of bags and loss of production material” cited by 75.0%;

- “Leachables and extractables” cited by 73.3%;

- “High cost of disposables” 68.8%; and

- “Material incompatibility with process fluids” and “We do not want to become vendor-dependent (single-source issues)” tied at 56.7%.

When asked about plans for bioreactors purchases, 70.2% of developer/manufacturer respondents reported they would specify SUS bioreactors for any new facilities at clinical scale and 51.9% for new commercial manufacturing facilities. About half of the respondents now expect to see fully SUS facilities in five years. Costs of SUS, much as with other bioprocessing supplies, are not a major concern, with purchasers willing and even preferring better products and willing to pay for a solid reputation, as long as the added costs are not unreasonable.

Figure 2 shows the 10-year percent increase in survey-reported average use (adoption) of SUS types of equipment within facilities. The largest growth rates involve big ticket items – bioreactors, mixers, membrane adsorbers and perfusion devices.

Conclusion

The dinosaurs, the largest-type stainless steel facilities, are not becoming extinct, but are dwindling in numbers, with fewer new ones coming online, with SUS increasingly replacing stainless steel. Classic, large scale, fixed, stainless steel equipment-based facilities will continue to dominate biopharmaceutical manufacturing, particularly at commercial scales and in terms of manufacturing volume. However, SUS currently dominates bioprocessing at pre- and sub-commercial manufacturing scales in most every other respect, and SUS is increasingly being adopted for increasing portions of new commercial products manufacturing. The SUS market will continue to grow, particularly in terms of revenue and process lines, including for commercial products manufacturing, a trend that is just starting.

References:

- Langer, E.S., et al, 15th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, BioPlan Associates, 511 pages, April 2018 (see www.bioplanassociates.com/15th).

- Top 1000 Global Biopharmaceutical Facilities Index, BioPlan Associates, at www.top1000bio.com

- Rader, R.A., “Biosimilars Paving The Way For Cost-Effective Bioprocessing,” Biosimilar Development, Aug. 23, 2017.

- Rader, R.A., Biopharmaceutical Manufacturing: Historical and Future Trends in Titers, Yields, and Efficiency in Commercial-Scale Bioprocessing,” BioProcessing J., 13(4), Winter 2014/2015, p. 47-54.

- Langer, E.S., et al., Advances in Biopharmaceutical Technology in China, Sept. 2018, 1228 pages.

Survey Methodology: The 2018 Fifteenth Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production yields a composite view and trend analysis from 222 responsible individuals at biopharmaceutical manufacturers and contract manufacturing organizations (CMOs) in 22 countries. The methodology also included over 130 direct suppliers of materials, services, and equipment to this industry. This year’s study covers such issues as: new product needs, facility budget changes, current capacity, future capacity constraints, expansions, use of disposables, trends and budgets in disposables, trends in downstream purification, quality management and control, hiring issues, and employment. The quantitative trend analysis provides details and comparisons of production by biotherapeutic developers and CMOs. It also evaluates trends over time and assesses differences in the major markets in the U.S. and Europe.

Author Biographies

Ronald A. Rader is Senior Director, Technical Research, 25+ years’ experience as a biotechnology, pharmaceutical and chemical information specialist and publisher. Editor/Publisher of the Antiviral Agents Bulletin periodical, the Federal Bio-Technology Transfer Directory, Biopharmaceutical Products in the U.S. Market. Mr. Rader has been Manager of Information Services, Porton International plc, Gillette Medical Evaluation Labs., MITRE Corp.; Technical Resources Inc.; and Bio-Conversion Labs. info@bioplanassociates.com, +1 301-921-5979, www.bioplanassociates.com.

Eric S. Langer is president and managing partner at BioPlan Associates, Inc., a biotechnology and life sciences marketing research and publishing firm established in Rockville, MD in 1989. He is editor of numerous studies, including “Biopharmaceutical Technology in China,” “Advances in Largescale Biopharmaceutical Manufacturing”, and many other industry reports. elanger@bioplanassociates.com, +1 301-921-5979, www.bioplanassociates.com.